JHVEPhoto

In our previous coverage of Rio Tinto (NYSE:RIO), we reluctantly handed it a “hold/neutral” rating as the exceptional downside risks from commodity pricing were offset by a very strong balance sheet. Today, we examine the recently released Q3-2022 operational review and update our ratings and price target on this company.

Rio Tinto Q3 2022 Operational Review

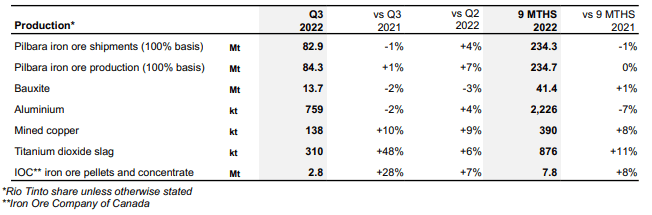

Production numbers were about in line with expectations and numbers ramped up versus the previous quarter.

Q3-2022 Operational Review

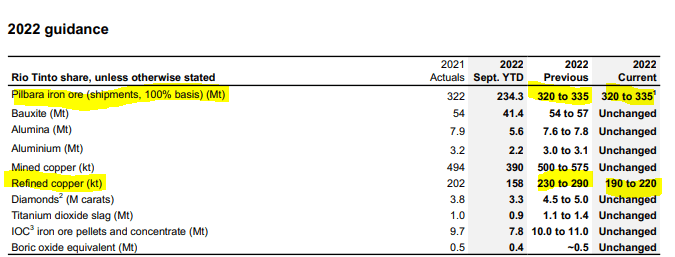

RIO updated its guidance slightly from H1 results and this included two small downgrades to their outlook. Iron ore production numbers, while still in the original range, were guided to the low end.

Q3-2022 Operational Review

RIO is trying to ramp up iron ore production at Gudai-Darri and Robe Valley while combating skilled labor shortages in both locations. Despite the higher costs associated with recruiting skilled labor, RIO did not increase its cash cost guidance for iron ore production.

Pilbara iron ore 2022 unit cost guidance of $19.5-$21.0 per tonne remains unchanged. Operating cost guidance is based on A$:US$ exchange rate of 0.71 and excludes COVID-19 response costs.

Source: Q3-2022 Operational Review

This has likely come about as the local price pressures have been offset by a very weak Australian dollar. Note that RIO’s guidance for costs is captured in US dollars.

On the refined copper side, Kennecott smelter and refinery materially underperformed, and this caused…