“A picture is worth a thousand words.” Now, it can also be worth much more in money.

Non-fungible tokens (NFTs) are digital artwork or media whose “ownership” is certified on blockchain technology, something similar to an electronic register. This ownership can be transferred and is often sold through auctions and trading marketplaces.

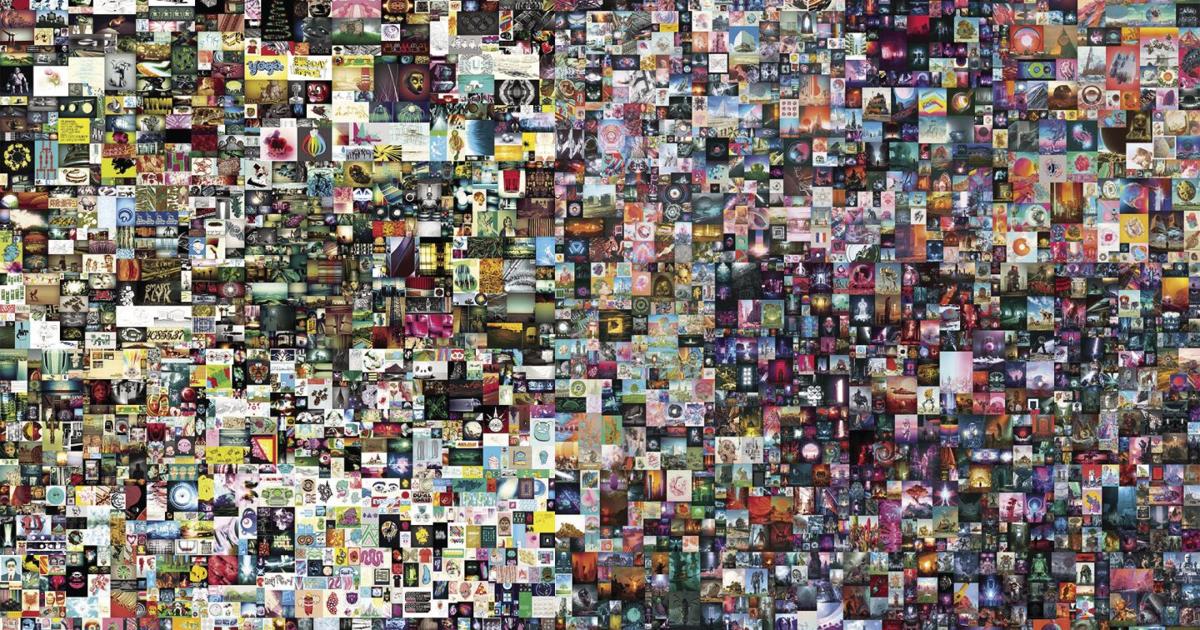

Although NFTs were introduced as early as 2012, the practice burst into the mainstream last year when artist Mike Winklemann — famous for creating a virtual piece each day — sold a collection of his “First 5,000 Days” for over $69 million. Since then, the largest trading platform, OpenSea, was valued at $13 billion in January.

However, the idea of NFT ownership can be misleading and a fuel for skepticism. The purchase of a digital asset doesn’t stop others from downloading and enjoying it, nor does it give the new owner rights over it, especially not copyright authority.

Often presented as a pointless waste of money, many NFT owners may disagree.

Rags to riches to lawsuit

One investor, Cooper Turley, put it simply in an interview with TIME: “It’s insider trading.” People purchase NFTs believing that their value will go up, hopefully leading to high future profits.

According to The New York Times, Izzy Pollak was one such person. Living with three other roommates, he decided…